Coursera: Practical Education in a Saturated World.

Coursera: Practical Education in a Saturated World.

There are two market environments I like to invest in.

Market A: This is a market ripe for disruption due to the current lackluster product or service being offered by the players in the space.

Market B: This is a new and growing market offering something of value that was previously not available.

Both of the above markets create a wide opening for a company to either update what is wrong or aggressively lead the way in a new and growing industry.

Coursera falls into market A. As businesses execute in market A, it allows them to scale into market B, providing the new standard that was once seen as the alternative. Coursera has the potential to be one of those businesses, etching away at the inefficiencies of the old, and creating a platform to embrace the new.

In order to disrupt a market we must first understand why the market is susceptible to being disrupted. When speaking about why education is sitting in a weak position, and susceptible to disruption, I will be referring to the United States.

College has become ingrained in America’s Culture. It is the first step towards independence in a young person’s life; a goal seen as imperative to creating a successful future. Those who work hard, and are granted admission to a school of their choosing, are rewarded with social networking, athletic events, quality education, and an overall productive and “fun” four years. Graduates exit well-rounded young adults, with a degree of proficiency in a field of their choosing.

Sounds like something worth participating in right? Unfortunately, like many comfortable institutions, colleges continue to slide into mediocrity when delivering on the important task of education, all while at a very high cost to the student.

Considering only the financial failures of higher-education, it becomes clear we have an educational crisis in America, an odd thing to have in a society where almost every piece of known information is a Google search away, at a cost of zero dollars.

We do not have an education problem, we have a “cost of certification” problem.

As of 2020:

Average annual public in-state tuition = $25,290 - X4 = $101,160

Average annual out-of-state tuition = $40,940 - X4 = $163,760

Average annual private tuition= $50,900 - X4 = $203,600

66% of students attend in-state public = 13,020,700 students

8% attend out-of-state = 1,609,300 students

26% attend private institutions = 5,150,000 students

Total annual expenditure per category:

= $329,293,503,000 for in-state public

= $65,884,742,000 for out-of-state public

= $262,135,000,000 for private

Total annual expenditure on tuition in America = $657,313,245,000

Current student debt is $1.57 Trillion.

*This is not sustainable*

Trade and vocational schools are already seeing success filling the void left by the shortcomings of higher education. Companies’ such as Lambda School, founded by Austen Allred, are doing an excellent job providing value to students at a fraction of the time, and cost. Lambda school collects no tuition upfront. Instead, you pay them back as you earn money at your new job. An incentive system perfectly aligned with a young professional looking to fill a spot in the workforce.

It is not only the financial burden that currently makes college unattractive, it is also the opportunity cost. Your early twenties are a time for personal development, goal setting, and hard work. You should be taking risks in your early 20s, shooting for the stars, and learning as you go. College does a beautiful job of delaying that. You receive four years of education, only to get spit out on the other end with debt up to your eyeballs, and a commoditized degree that has you starting at zero with most employers. Learning starts when you enter the workforce, when problems have to be solved, and customers’ needs must be met. There will always be certain academic powerhouses such as Stanford and Harvard, offering value due to the universities’ brand, and internal network. You will just have to pay-up.

For the majority of students, higher education is an overpriced product that stunts growth through opportunity cost, and the eventual burden of debt. But, I do not see college being disrupted quickly. These institutions are embedded in our society. Higher education received $1.07 trillion in federal funding in 2018. A similar amount of $1.2 trillion was spent towards funding hospitals. Disrupting institutions with this type of financial backing and ingrained societal standing will not be easy. So, what does one do when seeking to improve the space through time and cost savings? You take the path of least resistance. For now, let’s keep the old playbook, but force their hand when it comes to efficiency, cost, and quality. Coursera’s approach of aligning itself with colleges, corporations, and governments to host their courses and provide optionality to their consumers is the correct evolution in education.

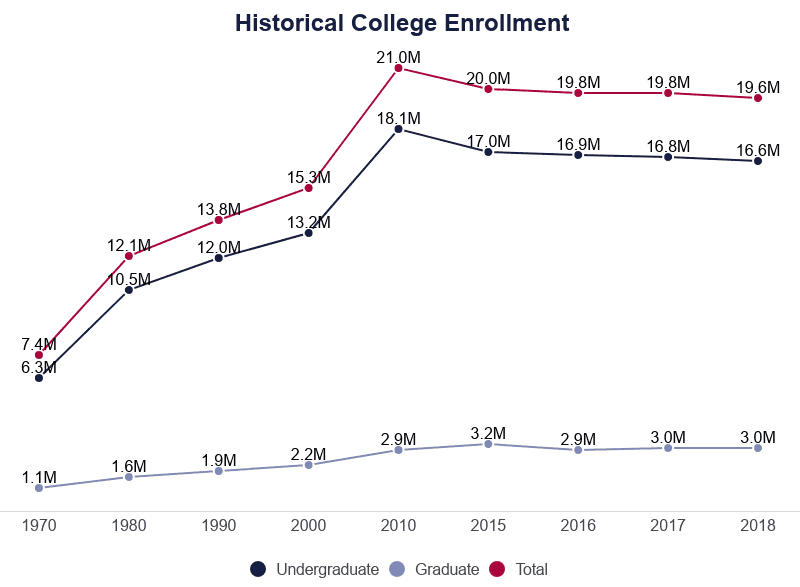

College enrollment is showing signs of stagnation, with degree enrollment down in 2018. Chart courtesy of educationdata.org.

Market Size

What is Coursera’s total addressable market (TAM)? The company reported in their S-1, “According to HolonIQ Smart Estimates, the current higher education market is currently sized at $2.2 trillion, and growing. The global online degree market was $36B in 2019 expected to be $74B in 2025.”

Another excerpt from their S-1, “We believe that we have a large under penetrated addressable opportunity ahead of us to enable the digital transformation of higher education and provide lifelong adult learning at scale.”

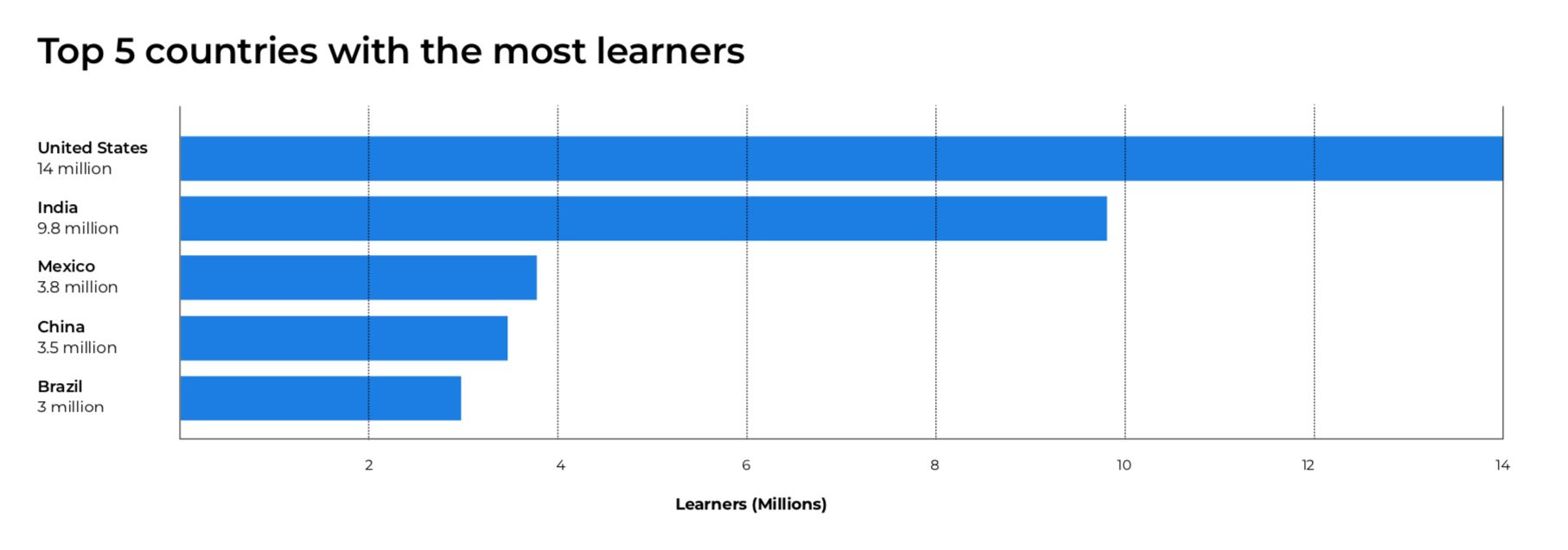

Given the numbers listed in the tuition breakdown, we are looking at roughly 20 million students enrolling in college, in America, per year. Coursera also reports that 51% of their revenues were generated from learners and institutions outside the United States during both years ended 2019, and 2020. There are roughly 190 million international students enrolled in higher education.

Current Learners per country (Top 5)

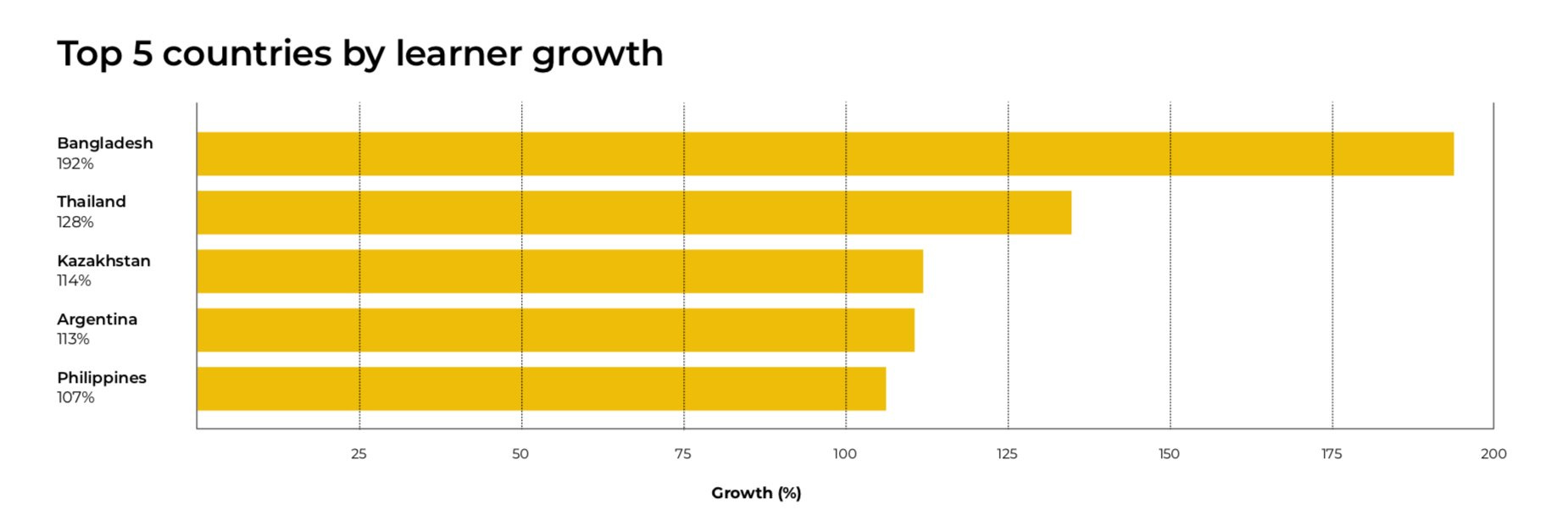

Fastest growing countries (Top 5)

Globally, this amounts to a total of 220 million students enrolled in higher-education.

It is projected globally that 1.3B people will reach working age in the next 10 years. Annually, this amounts to 130M new workers entering the workforce over the next decade. Coursera offers job ready certificates to people with zero industry experience. Those looking to obtain an in-demand job fit into Coursera’s total addressable market.

Finally, we have those who are currently in the work force. Either with a masters degree, bachelors degree, certification or high school diploma. How can Coursera service these people?

According to the World Economic Forum, “95% of U.S. employers plan to retrain existing employees in response to shifting skills needs in 2020.” Yes, you read that correctly, 95%. We currently have roughly 157 million Americans in the work force. If 95% signed up for guided projects, courses, or specializations, that would amount to 149 million new learners for Coursera, an increase of 93.5% of learners in America. With a fast-paced, technologically driven economy, education spanning fours years in your early 20s will not suffice.

Coursera not only fits the needs of a more efficient, lower cost alternative to college, it fits the needs of working professionals needing to modernize their abilities to stay competitive.

With 51% of Coursera’s revenue coming from outside the United States the last two years, developing countries obtaining better internet connectivity (currently 4.66B active internet users) will be another factor behind this company’s ability to reach more learners. If this trend persists, we could continue to see triple digit growth in registered international learners.

Americans take what we have here for granted, but a 20 something in India, or Bangladesh being able to take an online class through Coursera, branded by a major American university or institution, is a value proposition that is truly life-changing. All great companies did one thing, create value. I can’t think of a more compelling and life-changing proposition than giving a person the ability to change their life through education.

Let’s break the numbers down on an annualized basis.

TAMs can be a large and fuzzy metric, often used to juice the bull side of an argument. It comes down to SAM (Serviceable addressable market).

220M higher-education students globally + 130M entering the workforce + 30M employed Americans + roughly 600M full-time international workers = 980M.

The 130M entering the workforce will overlap with those currently enrolled, or soon to graduate University, so that estimation is likely high.

Over the next 5 years we are looking at a total SAM of roughly 4.9B people.

What’s interesting practically anyone could make the decision to sign up for Coursera in some capacity. What is more paramount than learning something new to better your life? Considering the services ease of access, and low cost, nailing down the SAM will be difficult.

If Coursera can capture 20% of the above annualized SAM, we are looking at 196M new learners, annually.

Coursera’s total registered learners was 37M, 46M, and 77M in the years ended 2018, 2019, and 2020.

We know we have a large global market, let’s look at Coursera’s offerings, and the fiscal and opportunity cost associated with enrolling in their programs. Remember, the only thing you cannot buy is time. Factoring in time spent to acquire a degree or certification is just as important, if not more important, than monetary cost. You can earn back the tuition spent, you will never gain back the time spent.

Coursera’s catalog:

1,000+ Guided Projects: Gain a job relevant skill in less than two hours for $9.99.

5,000+ Courses: Learn something new in 4-6 weeks for free, or at a cost up to $99.

550+ Specializations: Gain a job-relevant skill in 3-6 months for $39-$99 per month.

40+ Certificates:

A) 25+ Professional Certificates: Earn a certification of job readiness for an in-demand career in 3-9 months for $39-$99 per month.

B) 15+ MasterTrack Certificates: In 3-12 months, earn a university-issued certificate from a module of a university degree and credit that can be applied to that degree in the future for approximately $2,000 - $6,000.

30+ Degrees: Earn a bachelor’s or master’s degree fully online for approximately $9,000- $45,000.

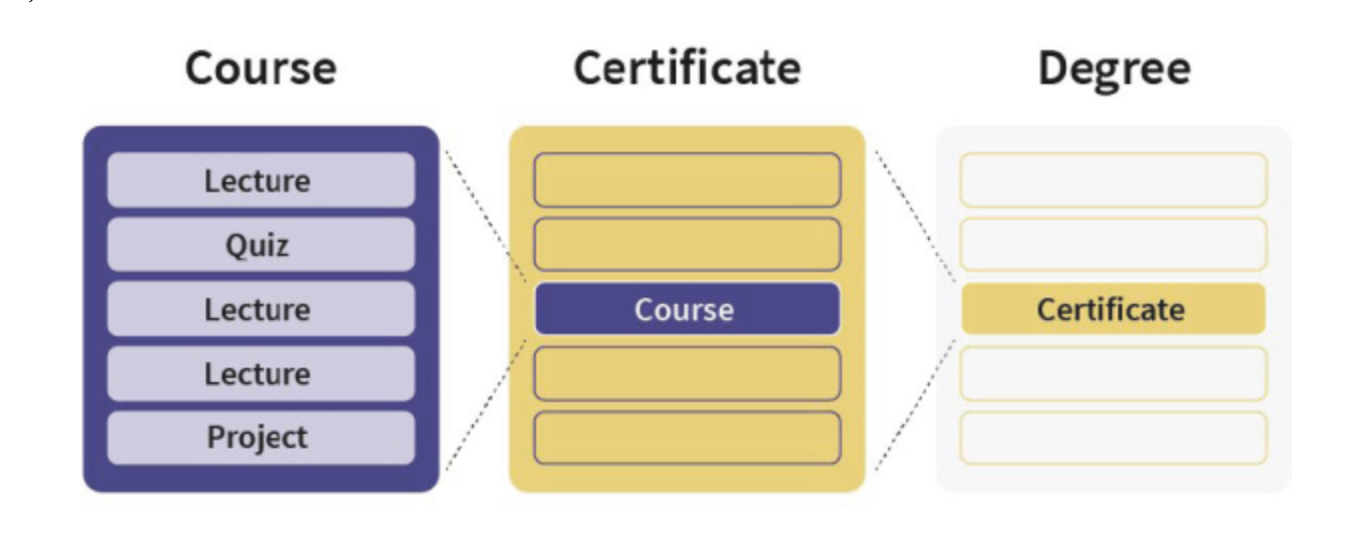

Programs are stackable—meaning one course can be applied to a certificate which can be applied to a degree. Below is an example from the company’s S-1.

“For example, a University of Illinois digital marketing course can count as credit towards a Digital Marketing Specialization, which could count towards a two-year MBA, all earned on Coursera.”

Not only am I impressed with the diversity of offerings, but also the ability to piece together a high-level degree due to course stacking. This is a very good idea, and addresses a few of the systemic problems of modern higher-education. Let’s touch on the latter first.

The drawback of modern education is the amount of time allotted to obtaining it. Almost nothing is left outside of school if a student wants to obtain a degree in a timely fashion. Once a degree is obtained, people start careers which then occupy the time previously filled by school. This makes it next to impossible to leave your current position if you want to go back and get a higher-level degree. Most people write it off completely due to the amount of time it takes, and the fact it will hinder, or kill their current occupation. With Coursera, all that changes.

For example, a person gets hired for an entry-level position at Google after finishing one of the Professional Certificates that Coursera offers through Google. That person could then slowly chip away at other certificates while working, adding to their skill set, while working towards obtaining a bachelor, or masters degree. This is a highly efficient way to practically teach someone without robbing them of their time, money, and ability to work.

Let's revisit the diversity of offerings in Coursera’s catalog. This is why it is hard to size up Coursera TAM, essentially anyone who is literate, curious, and has an internet connection is a potential customer (on a global scale). Competing with an overpriced college system is one thing, but providing governments and companies the ability to quickly and efficiently re-train employees is a very useful service. Not only does it save these institutions millions in hiring fees, but it also retains their existing employees who are familiar with daily operations. Coursera also benefits from free marketing every time an institution choses them to train employees. I discussed the numbers above, but servicing people already in the workforce whose jobs could be at risk due to the fast pace nature of our technologically driven global economy, is as much an opportunity as those looking to enter the workforce.

Lastly, I want to discuss blended learning. Below is an excerpt taken from the company’s S-1 on the subject.

“We believe the future of education will be characterized by blended classrooms, job-relevant education, and lifelong learning, and that online learning will be the primary means of meeting the urgent global demand for emerging skills. According to an estimate by the World Bank, there were more than 200 million college students around the world as of October 2017, many of whom did not have necessary job-relevant skills. Online learning holds the promise to enable anyone, anywhere to learn new skills in preparation for high demand, digital jobs. The combined forces of online learning and remote work have the potential to increase global social equity by enabling a future where anyone, anywhere has access to both high-quality learning and high-quality job opportunities in an increasingly digital world.”

Another excerpt pertaining to blended learning from the company’s S-1.

“Colleges and universities can use Coursera for Campus to deliver branded online learning at low cost in a new era of financial challenges for higher education and evolving student preferences for hybrid learning. Coursera for Campus enables universities to leverage our global online learning platform to provide job-relevant, credit-ready, high-quality learning at higher scale and lower cost than in-classroom learning alone. Accelerated by the pandemic, thousands of higher education institutions launched Coursera for Campus over the past year, making it one of our fastest growing offerings. As of December 31, 2020, over 130 colleges and universities were paying customers of Coursera for Campus.”

The immense amount of federal funding colleges receive, as well as their standing in our socioeconomic system, will make the evolution of education a slow and steady one. This is not an easy area to change. It does not come down to learning, everyone is free to learn at any time, from just about anywhere. It is the public’s acceptance of alternative credentialing that is going to take time.

Blended learning is an important aspect of Coursera’s growth strategy. Instead of giving a binary option of college or online, it allows students to attend a university and take a mix of both in person and online classes. This lowers students costs, and allows them to participate in the aspects of college that make it compelling in the first place. Again, Coursera does not need to totally disrupt the industry for it to succeed, an update will suffice. I believe blended programs will see wide adoption in the coming years, a smart move by Coursera.

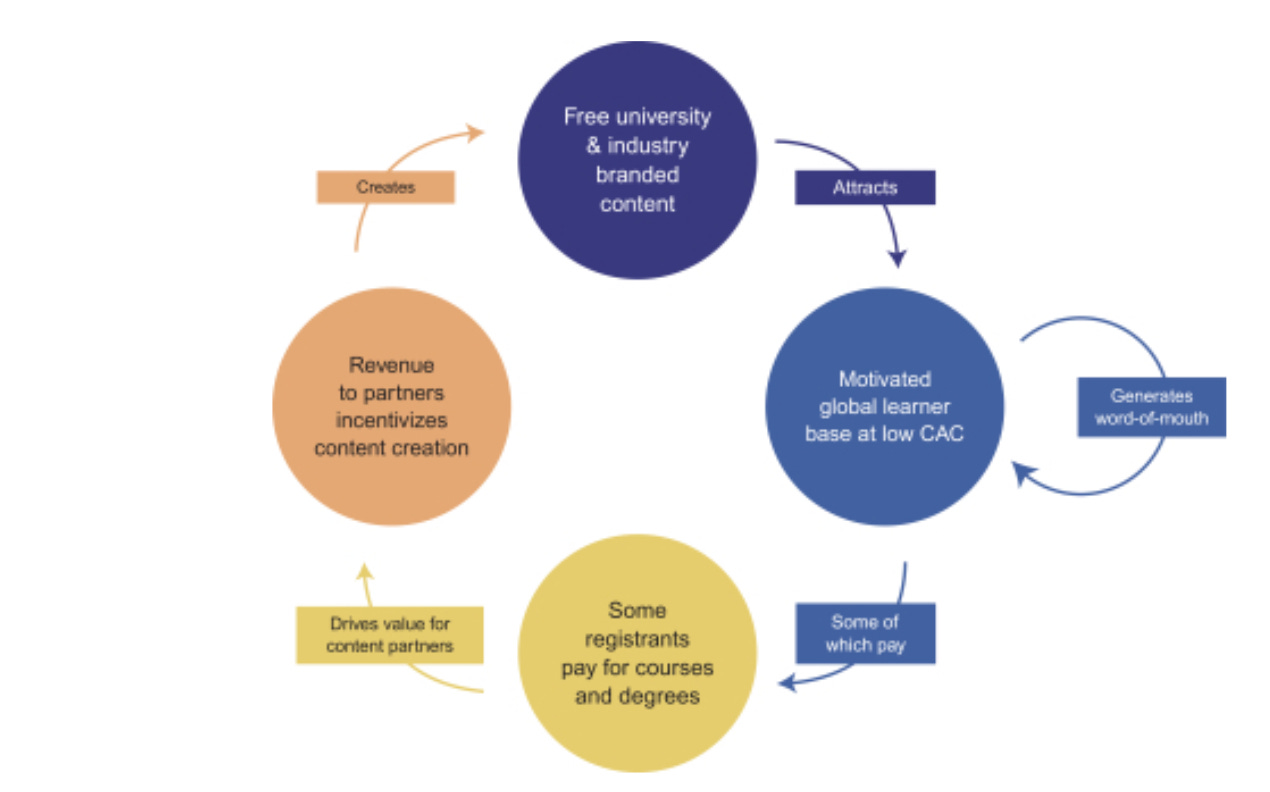

Flywheel

Imagine this scenario: You just finished your four-year degree at a respected college, and began working at your first real job. You begin to meet your co-workers, and one of them tells you that they obtained a bachelor’s degree at half the cost, while working or traveling. Or, a co-worker took a career ready Professional Certificate through Coursera, and six months and $240 dollars later, has the same position as you. Surely this would make you rethink the role universities play in helping people obtain a job. It might even make you visit Coursera’s website to see what offerings could benefit you and your future. Promotions, pay-raises, and even new careers are all a possibility with Coursera’s services, at both a fair monetary, and opportunity cost.

Below is an excerpt from the company S-1:

“Network of leading academic and industry partners: Our large and global learner base attracts top-tier educator partners by allowing them to reach new audiences and create new revenue streams with relatively small up-front investments. We carefully select our university and industry partners, prioritizing quality, subject expertise, and geographic appeal. As technology advances and new relevant skill sets emerge, our growing partner relationships enable us to be responsive in providing in-demand skills for aspiring and ascending professionals.”

Adapt or die. Academic institutions are seeing the change, and realizing Coursera is offering them a way to modernize how they do business. In the same sense, the industry partners are finding a way to circumvent some of academia, allowing them to pool their own potential hires by educating directly to the public without the need for a middle man.

Competition

Inefficiency creates opportunity, and it seems people are awakening to the problems associated with educating our youth. There is quite a bit of competition in this space, but I view this as a positive (for now).

When you are in the early-innings of a new industry, competition is confirmation you are fishing where the fish are. The key here is being early. If you arrive by the time market shares have been captured, it makes for a very difficult endeavor (the fish have been caught).

When you find an industry that is young, and filled with potential, it is very likely to produce many winners. Think of all the amazing software companies that came to be in the last 10 years. You didn’t have to pick just one to make a successful investment in the space. Many were rewarded by providing the right product at the right time.

I believe this is the situation we currently have with Coursera. We are in the early innings of online education. We have the technology to do it, all we need is the public to be open to it. Second, there will be more than one winner within this industry. The old model is not sustainable, and as soon as people realize education is something they can acquire on their own time without going into debt, the idea of what is possible will make students pivot towards the alternative.

Below is a list of businesses in either direct or indirect competition with the products offered by Coursera, courtesy of their S-1.

Direct-to-consumer, online education companies: 2U, Inc., edX Inc., Eruditus Learning Solutions Pte. Ltd., FutureLearn Limited, Udemy, Inc., and upGrad Education Private Limited

Corporate training companies: A Cloud Guru Ltd., Degreed, Inc., LinkedIn Corporation through its LinkedIn Learning services, Pluralsight, Inc., and Udacity, Inc.

Providers of free educational resources: Khan Academy, Inc., The Wikipedia Foundation, Inc., and Google through its YouTube services.

When thinking about competition, Coursera has a few advantages that stand out.

Brand name.

High-quality founders with high standings in academia.

High-quality partners both academic and institutional.

Number of courses provided

Number of partnerships.

In an easily accessible online marketplace it is going to come down to quality of partnerships, and the trust and recognition associated with the brand. Google had a lot of options when picking who to partner with when launching Google Career Certificates. Courses that offer training in high-demand jobs such as Data Analytics, UX Design, IT Support, and Project Management. Google chose Coursera.

A few honorable mentions that have partnered with Coursera to provide students, and current or future employees with online education include: Yale, IBM, Intel, Microsoft, Stanford, Unity Software, Amazon, Autodesk, Duke, Facebook, and National Geographic.

I believe YouTube is the most valuable educational tool currently available at scale. The only problem with YouTube is after watching a video, you can’t be awarded a credential. Speaking for myself, I have learned a great deal from YouTube. The problem is proving your competency when there is no measurable standard. Coursera solves the biggest current problem with education: costs, and credentials. We don’t have a problem finding teachers and information, it is the problem of convincing employers the information you received was valuable, and learned and retained to a high-standard.

Founding & Management

Coursera was founded in 2012 by Andrew Ng and Daphne Koller, both computer science professors at Stanford University. They began experimenting in 2008 with a MOOC program called SEE (Stanford Engineer Everywhere). These free online courses focused on machine learning, and where taught by Ng himself.

Ng and Koller realized the importance of the content they were teaching, and wanted to be able to reach a larger audience. The courses launched during the SEE program saw over one hundred thousand people register for the course globally, inspiring Andrew Ng to continue pursuing high-quality online education for everyone. Andrew wrote a fantastic letter in the company’s S-1 where he stated, “I was teaching 400 on-campus students a year at the time and realized that to reach a similar audience, I would have to teach for 250 years.” They began to record more lecture videos, add in complimentary features to better the classes, and with a bit of momentum and time, Coursera came to be what it is today. Andrew Ng remains with the company as chairman, and Daphne Koller left Coursera in 2016 to work at a biotech company.

The company is currently being led by CEO Jeff Maggioncalda. Jeff has been CEO since 2017, and holds an MBA from Stanford University. Jeff was the CEO and co-founder of Financial Engines. FE provided online financial advice to those close to retirement. The company was co-founded by Nobel Prize winner William Sharpe, and saw great success under Maggioncalda’s 18 years of leadership as CEO. Maggioncalda’s track record, and the brains behind the founding partners, shows Coursera was not only founded on a flat and stable foundation, but those who dreamed up the future of education selected a fine man with a good track record to lead the company.

Something interesting to note about Coursera. The company was not founded by a disgruntled college dropout seeking a better educational experience, but by a pair of highly respected professors at one of the top academic institutions in America. Ng and Koller saw a better way forward within the belly of the academic world. For me, this adds validity and legitimacy to the long-term vision of Coursera.

COVID-19

Last year threw a wrench in the gears, making it hard to discuss a business without discussing COVID’s affects on its operations. Coursera was one of the companies that benefited from the disappearance of in-person gatherings. It is easy to think of this company as lucky, being positioned like it was pre-pandemic. I would argue the opposite. Forward looking companies have a knack for welcoming worldly vicissitudes, such as the hard working individual welcomes luck. The pandemic pulled the curtain back on societies’ inefficiencies, one of them being education. The $1.57 trillion in student loan debt existed pre-COVID. The gig economy many Americans under 30 find themselves in existed pre-COVID, and the complacent universities with teachers passively going through the motion on tenure, also existed. This rug pull helped shed light on the quietly accepted stagnation of academia in our society.

With the continued partnerships, and growing learner base, I believe the COVID boost Coursera received will last. This unfortunate event has, and will continue to propel Coursera forward with not only a label of endurance, but of service when it was needed the most. Would online education be as well known and adopted right now if COVID never happened? No. But, would it have slowly grown due to the positive alternative it offers? Yes. It is my belief that Coursera is not only here to stay, but will morph into an integral part of the global online learning ecosystem.

Operations & Financials

How does Coursera make money? First, I want to mention that Coursera is certified as a B Corporation. A Certified Benefit Company is a company that meets certain criteria of social benefit, and aligns its values with having a positive impact on humanity. Essentially, Coursera has a legal duty to balance shareholder needs with the needs of society. Companies registered as B corps align themselves with high environmental standards, transparency, etc. It’s an obligation that the business is not only creating value for shareholders, but to those whom it serves. The business has to go through an assessment to be officially certified as a B corp, and must maintain these values through operations. I do not see this having any effect on the company long-term. Truth is, unless you provide your customers with value, you no longer have a business to run, B corp or not. The value Coursera provides to people of all walks of life through its operations is quite obvious. I don’t see the need for a label to be attached, but nonetheless, I am happy they recognize the importance of ethical value creation.

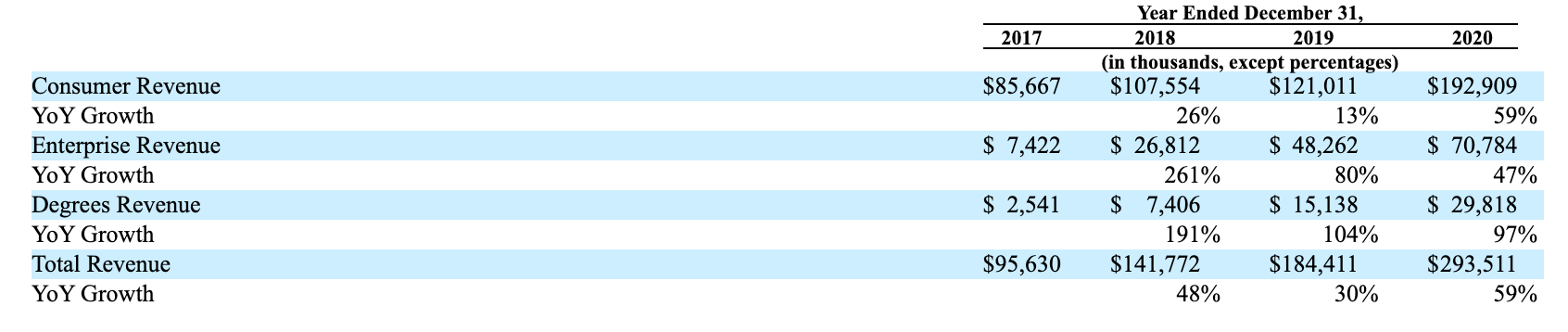

Coursera defines revenues as three categories.

Consumer Revenue—This revenue is generated when someone signs up for a paid course on Coursera. Generally, there is a 7 day free trial, then either a single payment is collected for shorter projects, or a monthly subscription fee is billed.

Enterprise Revenue—This is sold as a subscription license to businesses, governments, and university customers. These enterprises sign on to three-year contracts, allowing them to host their content on Coursera. This allows users to enroll in their branded courses in order to receive a certification.

Degree Revenue— This revenue is generatedthrough Coursera offering a university’s degrees on their platform. Coursera earns a service fee that is based on total tuition collected by the university. The university is a customer of Coursera’s online offering, and the amount is paid to Coursera each university term.

Total registered learners grew 24% YOY in 2018, 24% YOY in 2019, and 64% YOY in 2020. The boost in 2020 was due to the COVID-19 pandemic.

Coursera has grown revenues annually at roughly 46% since 2017.

Coursera currently has $285.3M in cash, and $24.6M in debt (healthy).

Paid consumers grew 61% YOY as of Q1 2021.

Paid enterprise customers grew 63% YOY as of Q1 2021.

Number of degree students grew at 81% YOY as of Q1 2021.

Net retention rate was 114% in 2020 up from 106% in 2019 for enterprise customers.

Below is a breakdown of YOY revenue growth per category.

Gross margin per category.

Degree margins sit at 100% due to no cost associated with creating learning material. The students pay tuition to the university, and a percentage of that tuition is paid to Coursera. Coursera recently stated in their 2021 Q1 call that they are seeing significant growth in learners signing up for professional certificates. A category that takes someone with no degree or experience, and equips them for an entry-level position at a cost of roughly $240. Ideally, this translates into people starting a bachelors degree while working their new job. This system of work readiness coupled with the ability to earn a higher-level degree is extremely attractive. It also sets up customers of Coursera to be filtered into their “degree students” section. A part of the business with 100% margins and lack luster competition.

Coursera is still not profitable, posting an operational loss of $66.6M in 2020. The company is taking the approach of investing in the business, trying to obtain as much market share as they can before opening the floodgates of profitability. Luckily, the company recognizes relatively high gross margins over their three revenue streams, with degree students being the standout at 100% GM. There is also very little maintenance cost associate with the platform, especially with the shorter projects and courses. Once added to Coursera’s website, these courses can be accessed by millions with no incurred cost to the business. This makes for a very scalable platform with the ability to accelerate growth through partnering with additional institutions and universities. This in turn will promote the company’s brand, grow their network, and produce even more attractive unit economics.

The company is currently investing in the platform to make the experience as engaging and functional as possible. A computer can never replicate a person teaching someone face to face, so this will be an area Coursera will have to focus on. Coursera is tackling this by shortening the time spent obtaining a certificate/degree, incorporating video lectures, and adding social aspects like course specific forums so students can exchange thoughts and questions.

Coursera published a blog discussing platform investments. You can read it here.

Given 51% of Coursera revenues are international, the company is focused on continued global expansion, offering those less fortunate an opportunity of a lifetime. They plan to continue to market their offerings and programs to individuals, businesses, governments, and academic institutions at a global scale. As countries develop, and a middle class begins to form and grow, we know a higher percentage of that income is allocated towards their children's education. If Coursera positions itself properly within emerging economies, this expenditure coupled with better internet access will help fuel future growth.

Coursera is continuing to grow their content and credential catalog, with the goal of creating the biggest and most reputable network of industry and university partners. Many of the projects and courses offered are free, hoping to convert their “freemium” enterprise customers into paid subscribers. If Coursera continues to provide value to these institutions by retraining, and bettering their existing employees, Coursera’s services could become an annual expense for these institutions.

Two interesting excerpts from the company’s S-1.

“Our production environment runs on a cloud, providing scalable storage and elastic computing. This architecture allowed our platform to effectively serve a 15x increase in registrations at peak hours during a pandemic-related surge in activity in late March 2020.”

“We invest substantial resources in research and development to drive our technology innovation and bring new offerings and features to the market. Our research and development team is responsible for the design, development, and testing of features and offerings on our platform. They are also responsible for building and integrating tools and systems to help our services function deliver high-quality service at lower cost as we scale.”

Valuation

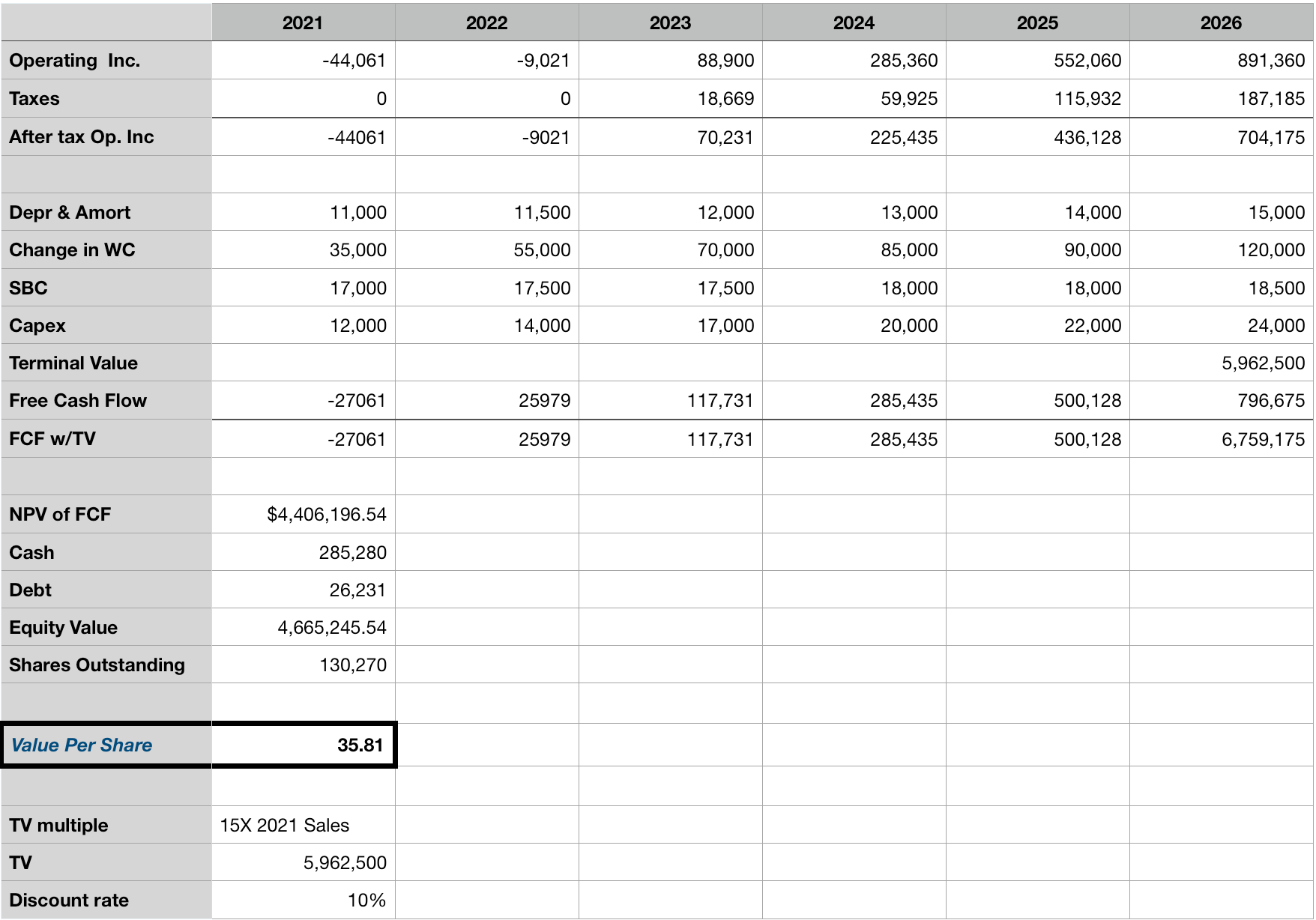

I use a discounted cash flow model (DCF) to see if I can make sense of the price a company is selling for. These are built entirely on forward-looking assumptions, and capture only quantitative value. The intangibles of today, become the value of tomorrow, having serious effects on top and bottom line growth. The problem is, they are hard to measure numerically. As a reminder, just because you can measure something numerically, does not mean you should allot more confidence to it. With that in mind, I try to make simple and conservative DCFs as a baseline to judge fair value. It’s important to know if the stock is priced for perfection, or selling at a discount to intrinsic value. But, it also depends on the company. Some stocks are always cheap, some are always expensive, and stay that way. Both can make good investments. Your level of understanding as to why the stock is cheap or expensive, and your ability to have a long-term mindset is more important than nailing the exact value of a business.

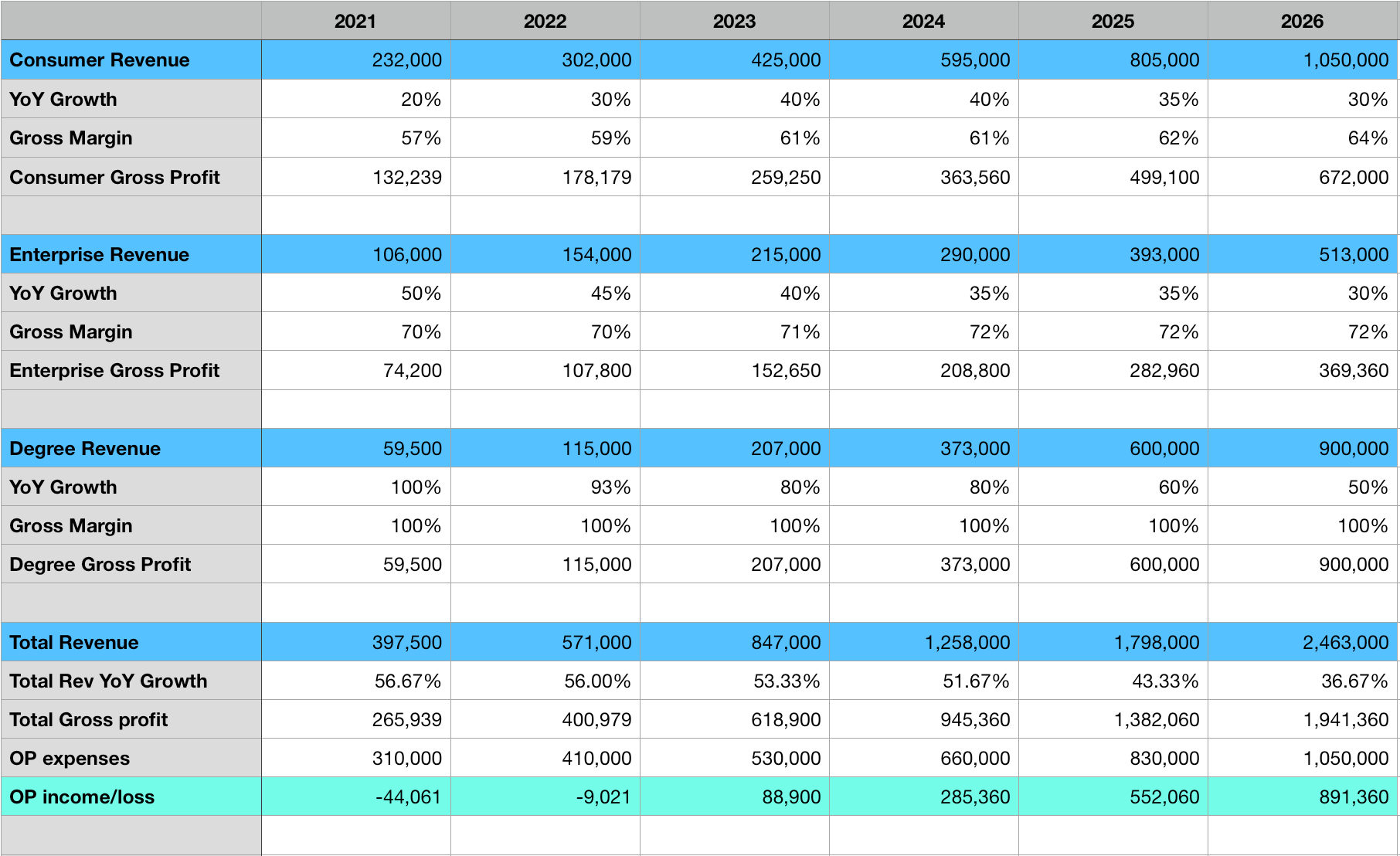

Revenue projection:

DCF:

Looking Forward

This is what makes investing hard, and why so many lag the index. Almost all asset allocation templates, financial figures, risk parameters, and current thoughts of business operations are derived from success and failure that took place in the past. It is very hard to make educated guesses about the future, and hold that conviction through volatility. Alas, that is investing.

First, on valuation. At the time of this writing (5/28/21) $COUR is trading at $38.00 per share. Based on my assumptions we know fair value is sitting right around current levels. Recently, we saw a significant sell off in growth names after a euphoric run that rolled over in February of 2021. While I don’t consider Coursera to be one of the popular high beta names, the company traded to euphoric levels shortly after its initial public offering in April of this year. It is standard for a lot of volatility to accompany a recent IPO, and with $COUR currently sitting near its lows, I took the opportunity to begin to purchase shares. I will be watching for the price to stabilize, and will continue purchasing shares at what I consider to be fair value. I don’t know if the stock will trade lower, but being able to acquire more shares in the high to mid 20s would allow for a nice margin of safety with viable long-term prospects.

Opportunity only exist if A: the opportunity is in fact an opportunity. And B: if it has not yet been recognized by others. When the opportunity has been recognized, the ROI drops significantly.

The opportunity with Coursera is the publics current view of education. People understand college is not the best solution, but their thinking generally stops there. The alternative is risky, and most parents don’t encourage risky behavior for their children.

Great companies that have not yet been recognized as such are the investments that yield the greatest returns. If Coursera is able to deliver on their promise of providing universal access to world-class learning to anyone, anywhere, the public’s view of education and credentialing will change. That mental shift, is where the opportunity lies.

I have long believed education is one of the ripest industries for disruption, just waiting for a better alternative. Because of this view, I have been looking for a company to fulfill that role in my idea of a better future. I invested in Chegg back in 2018, hoping it would continue to help students by cutting costs, and providing a network of tutoring. That investment has worked out well, but Chegg simply lends a helping hand to the current model of education. It is not in the business of providing students with a better alternative. Chegg’s value creation is in helping those get through college, not providing a better alternative. I like it, but I don’t love it.

Coursera is the business that has the potential to not only make a positive impact on people, but to provide stiff competition to the expensive, and complacent institutions that are failing in educating our youth. With the added services of certificates, projects, and specialization to help re-train and make those working more competitive, I can’t help but think Coursera is the company I have been waiting for. And not just for America, but for the world. A company that allows you to have control of your future without squandering graduation with the realization of the debt recently incurred. A company that will provide a specialization for someone not well versed in technology with the opportunity to update their abilities in order to provide for their family. A company that allows a young man in a developing country to take a course offered through Google or Stanford. Name a better value proposition, I will be waiting.

Disclaimer

The opinions and views expressed in this article should not be taken as professional investment advice. Market speculation is very risky, and you should do your own research before deploying capital. Any action you take upon the information provided on this website is strictly at your own risk.

Disclaimer

I am long shares of Coursera ($COUR).