The Risk of Mitigating Risk

Investors should always be thinking about risk. And when thinking about risk, it is important to distinguish between risk that is in your grasp to mitigate, and the inherent risk of doing anything. You should also think about how much of your future you are constricting in the name of risk management today. If good investing in businesslike, and Mr. Market is an irrational and temperamental entity, what risk is measurable and sensible in the face of a volatile environment?

As I am writing this, it is 9:10AM on a Saturday. The birds are chirping, the sky is wide and without a cloud, and everything is still. And yet, only a month ago, the mountains surrounding me were on fire. Helicopters and planes ripped through the sky as people put their belongings into their car in anticipation of an evacuation. The air was buzzing, the stress within the neighborhood was palpable, but not today. Today everything is going just fine.

During fire season, one of my neighbors will regularly climb onto her roof and water the house down in the hope of retarding an ember floating onto her house and igniting the roof. A lady, in her late 50s, crawling around a wet and slippery roof, in order to prevent risk. A fire possibly reaching her house and burning it down is an environmental risk she cannot control, and insurance in due time will make everything okay. But, slipping and falling off your roof from forty feet in the air and being put in either a wheelchair or a casket, is real risk. Self-inflicted real risk.

So, what is risk if only recognizable once a threat? And what is risk when you are the one creating risk, to deal with risk in the future, which might never materialize? Dealing with risk properly is a balance of doing, and of not doing. If you are crippled by the fear of risk, you might never leave your house. If you are too proactive, you might slip and fall off your roof.

In this essay I am going to discuss what I see as environmental risk (you get this when doing anything), risk you can mitigate, and self-inflicted risk (risk you create). To make this point I constructed three portfolios on December 31, 2019. I held these three portfolios through the COVID crash and liquidated all the positions on December 31, 2020. All three portfolios were 100% invested and evenly distributed among 20 businesses. No leverage was used, as I view leverage as created risk. I consider all the businesses selected in each portfolio to be best in class. The only main difference is their risk profile and beta.

Let’s start with portfolio 1. Portfolio 1 is filled with high-quality businesses that have a long and successful track record, competent management, positive cash flow, and are leaders with a strong competitive advantage in their industry. I would consider them to be quite low risk to reward, considering the businesses’ historical returns. Let’s see how Portfolio 1 did.

Portfolio 1 returned 25.95% compared to 16.26% for the S&P 500, an outperformance of 9.69%. The S&P 500 saw a peak to trough decline of 35.34% while portfolio 1 declined 37.02%, a difference of 1.68%. Outpacing the index by 9.69% for 1.68% more volatility is a fantastic long-term trade-off. These companies represent some of the best in the market, and so far the lesson is that when panic hits, everything gets hit. But, the better companies turn around faster, and subsequently outpace the index. Boeing was hit particularly hard, and Portfolio 1 would have returned 29.12% with a maximum drawdown of 35.05% with Boeing not included. A small detail that would have Portfolio 1 beating the index by double digits with less volatility.

Next is Portfolio 2. This portfolio has, in my opinion, some of the best growth names in the market. These are companies leveraging technology to disrupt huge markets, growing fast, and run by some of the best, and brightest of our time. These companies all sell at a premium, and have more beta than portfolio 1. This portfolio is viewed as higher risk.

Portfolio 2 returned 253.97% in 2020 compared to the Nasdaq’s return of 43.64%, an outperformance of 210.33%. The Nasdaq saw a peak to trough decline of 30.2% while portfolio 2 declined 45.6%, a difference of 15.4%. Outpacing the index by 210.33% in exchange for 15.4% more volatility is something dreams are made of. Last year was an anomaly in two ways. First, COVID was one of the fastest and most panic filled market crashes on record. A true “the world could possibly be ending for a while” scenario. Second, the effects of COVID affected many of the above companies in a positive way, accelerating our destiny with the future, and thus, the mission of these businesses. I still believe these companies would have outpaced portfolio 1 by a wide margin without COVID, just not this extreme of a gap.

I wanted to test these portfolios through 2020 because they show a perfect example of environmental risk. A type of risk largely outside investors’ control. What the above backtest shows is that when s#@*t truly hits the fan, everything gets their fair share of panic. There are a few outliers, but no one was looking at them and saying “these stocks tend to do better in a pandemic.” COVID was like a wildfire rushing towards everyone, and as long as you didn’t slip off your roof in a panic, things turned out okay. I know of only one investor who liquidated his entire portfolio prior to COVID and that was Ben. Reports were coming out of China that did not look good a few weeks before panic set in here in America, and subsequently, the markets. Ben has a background in molecular microbiology, which I’m sure played a role in his decision to liquidate. Ben made the perfect call, but what is even more impressive was his ability to buy back at market lows. It’s one thing to call the top, and a whole other beast to buy the bottom. You have to play both correctly, or your decision to sell was in vain. I sat there and held my fully invested five stock portfolio though the panic. My decision was simpler, and didn’t require me to buy when the world was melting all around me. Ben was able to do so, and reaped the rewards. But, if Ben had decided to sit in cash for just a few weeks, or a few months longer, he would have been buying everything he previously owned at much higher prices, lowering his annual return. I did nothing and it worked out just fine, Ben reacted perfectly and returned a staggering amount in 2020. COVID was a manifestation of pure panic in the markets. I hope we don’t get another pandemic in my lifetime, but we surely will get panic in one form or another.

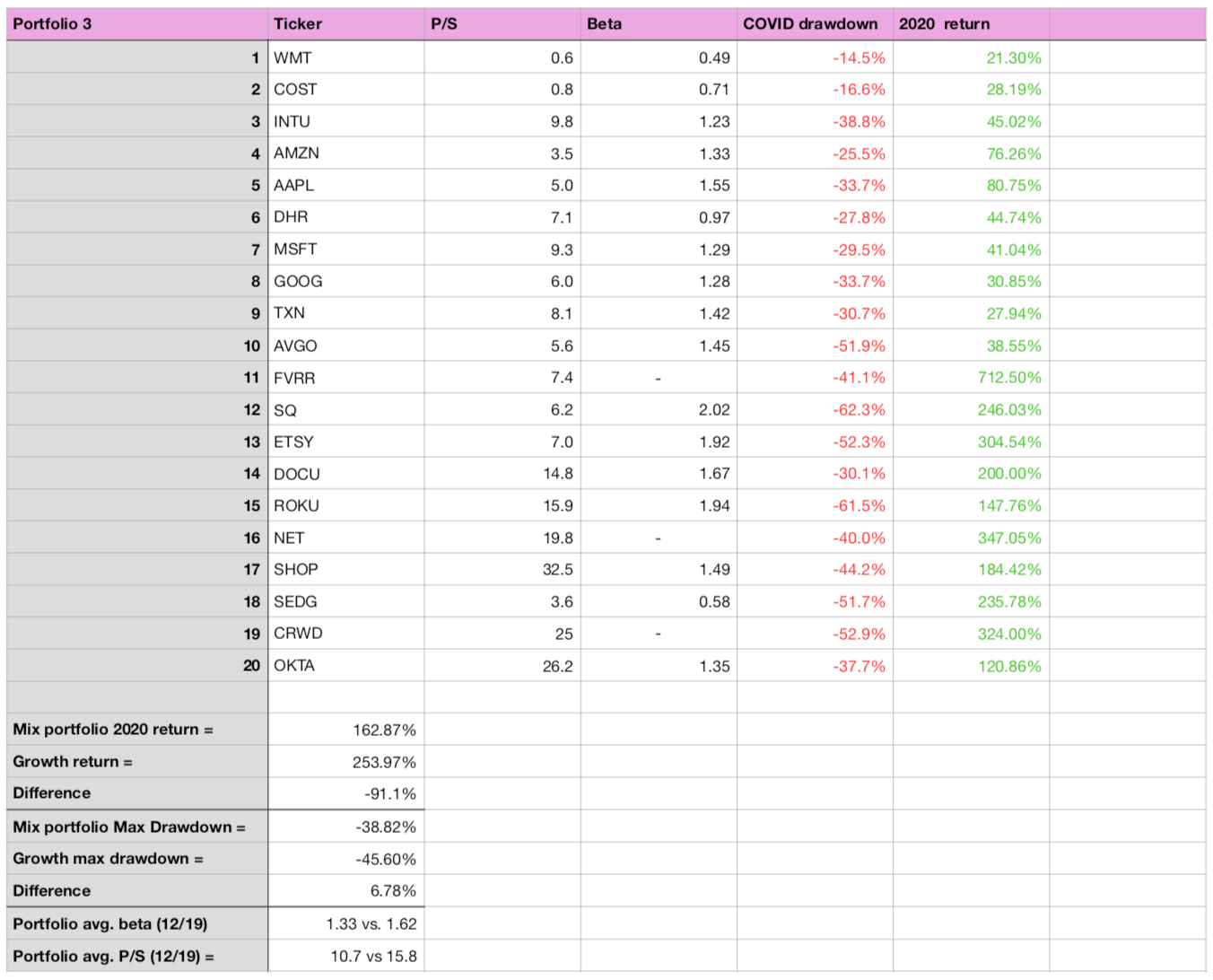

Finally I decided to blend these two portfolios. Could I lower my volatility without squandering my long-term results? Lets see…

Well, unfortunately the answer was a resounding no. Even when I picked some of the better names from portfolio 1 who had lower volatility than the market, and outsized returns, it still dropped the annual return by 91.1%, with only 6.78% less volatility compare to Portfolio 2. As I like to say, your risk management of today will be your underperformance of tomorrow.

So, what are the lessons here? After looking at each portfolio, you might want to shove all your money into high-quality growth stocks, but that is not the lesson of this exercise.

The lesson here is you can’t truly prepare for environmental risk, or conclude that less volatile stocks will respond better in a time of panic. Look at Boeing, who would have thought a monopoly like Boeing would drop 74.4% while almost all high beta growth names plunged “only” 40%.

Lesson 1: Environmental risk (macro).

This risk is hard to predict, and even harder to construct a portfolio around. I believe it is best to take the blows that the market, and the world, throws your way. Everyone else is hurting too, just don’t be the one who reacts to it. Better days are ahead.

Lesson 2: Watering your roof.

If you do see some environmental risk, make sure you are not jeopardizing your portfolio in the name of risk management. There are sensible ways to mitigate risk, and insensible (usually complex) ways of transacting too much, and thus limiting your long-term portfolio’s performance. Ben is the obvious exception here, he had to sell perfectly, and buy back in when the markets were melting. My advice is to keep it simple, don’t be a hero, and maintain the mindset of a long-term business owner.

Lesson 3: Risk you CAN control.

Looking at the backtested equity portfolios, it is quite apparent the best indication of resilience to environmental risk is to own high-quality, forward-thinking companies. Costco was one of the standouts, even without being a technology company. Costco held up very nicely, declining only 16.6% and finishing the year with a gain of 28.19%. Costco is an exceptional business, from the way it is structured, to management, to their exceptional customer service, and value proposition. These were the clues pre-COVID that you had a company in a defensive stance to worldly vicissitudes.

Lesson 4: Valuation is no indication of risk.

Many of the highly valued companies in Portfolio 2 had drawdowns similar to that of the less expensive and more stable companies in Portfolio 1. Do not equate expensive with risky.

Lesson 5: Portfolio construction.

Creating a portfolio from the top down, and fitting assets into that portfolio’s risk parameters is based purely off those assets past performance. As we can see when markets crash, it all crashes. I believe it is best to build a portfolio one stock at a time, and stress test each business through environmental risk, not through asset allocation. Volatility is not risk, risk is you not understanding a business well enough to see when it starts to derail. As a bottoms-up investor, the risk you can control is your vigilance towards the businesses operations, and your understanding of the economic environment it operates in.

Market returns come from a small number of stocks, and a small number of days within the market. According to this article, “The best-performing 306 companies (just 0.5 per cent of the total) accounted for almost three-quarters of the wealth created by stock markets over the last 29 years. The best-performing 811 firms – 1.33 per cent of the total – accounted for the entire amount.”

Risk is not owning these businesses, or selling them due to short-term volatility. Risk is owning too much in the name of safety. Risk is trying to stop an inevitable and temporary side-effect, and in turn, hindering your performance.

It is your job as an investor to pick one stock at a time based on its FORWARD looking risk profile. We saw how durable and forward thinking companies dealt with COVID after the panic subsided, they rebounded, some even doubling, or tripling. This backtest for me solidified that I want to do my very best when it comes to owning the strongest, and best managed companies for the long-term. There will be times of pain and confusion, but that is life. The best and the brightest find a way to keep pushing forward.

So what is risk? An unwelcomed future event showing up earlier than expected?

This was great Nick.